Crossing the Event Horizon on Labor and Wages

Why the Wall Street Consensus Underestimates Wage Pressure in 2024 & Beyond

Over the years, I have tended to think of aging demographics as the white noise on the radio… the snow on an old TV… the hiss that expands inexorably through the universe from the Big Bang (no pun intended on the GI Generation’s behavior following their return home from WW2).

For their part, investors seem to acknowledge that demographics matter in the long run, but the rate of change is so slow that the subject nearly always ends up as an afterthought — a bullet on some investment slide deck or Sparks Notes under “Structural Tailwind.”

I remember when Druck went on a 2013 tour to warn college kids about the catastrophic math from an eventual explosion of government liabilities as the Baby Boomers would one day begin to draw social security and consume healthcare in droves. Last year he hit the road again with “it’s worse than I imagined.” It made for a few retweets and discussions in macro circles…and then everyone promptly turned back to Nvidia speculation by day, and Season 3 of Mandalorian in the evening.

We all know the Boomer trend is coming to a head in the next 10-15 years on the fiscal side, but investors are underappreciating the impact today on employment and wages. The clearest example has been watching Recession Bros swear up and down for over six months that a rip to 350k+ initial jobless claims and 5% unemployment (oh the horror) is nigh… “maybe not next week, but we are right there.”

Some data for context:

The 70 million Boomers (1946-64) who are still living of the original 76mn born will be 60-78yrs old this year (the ~18mm who died since birth were offset by ~12mn immigrants following the liberalization of national-origins quotas with the Immigration Act of 1965).

US births by year:

Source: CDC National Center for Health Statistics

The table above highlights a birth plateau of ~4.2-4.3mm/yr during 1956-61. The “Plateau” Boomers are 62-67 years old this year, and the median is now 65.

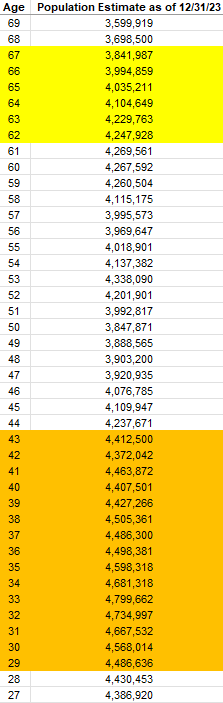

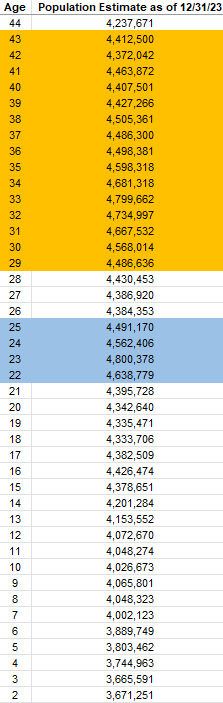

This squares pretty well with US Census estimates that show total population by age as of 31 December 2023 (table below). I have highlighted the Boomer Plateau bulge in yellow, and you can see their Millennial children coming up behind them in orange:

Source: US Census

Bottom line: the median US Boomer turned 67 sometime in 2023, and the tip of the spear from the “Boomer Plateau” will turn 67 sometime in 2024.

Now, it seems there are many professions where you can toil well into your 80s (politics comes to mind), but certain professions simply will not permit this. For instance, the FAA under 14 CFR Part 121 will not allow commercial pilots to fly for a carrier once they reach age 65. The House voted to raise this requirement to 67 last summer, but passage has been stalled in the Senate, and in any case the ICAO (International Civil Aviation Organization) will not permit international flights piloted by 65+ pilots. This is a key factor in why flight crews received 34%+ 3-year raises last year. I remember reading about the looming pilot shortage over a decade ago when I received a private pilots’ license. The industry was already warning about this back then, but it took over ten years for anyone to care. The forcing function was a wage shock. Now everybody knows that everybody knows that pilots will crush it for years to come. The markets seem to need a slap in the face to get the picture though.

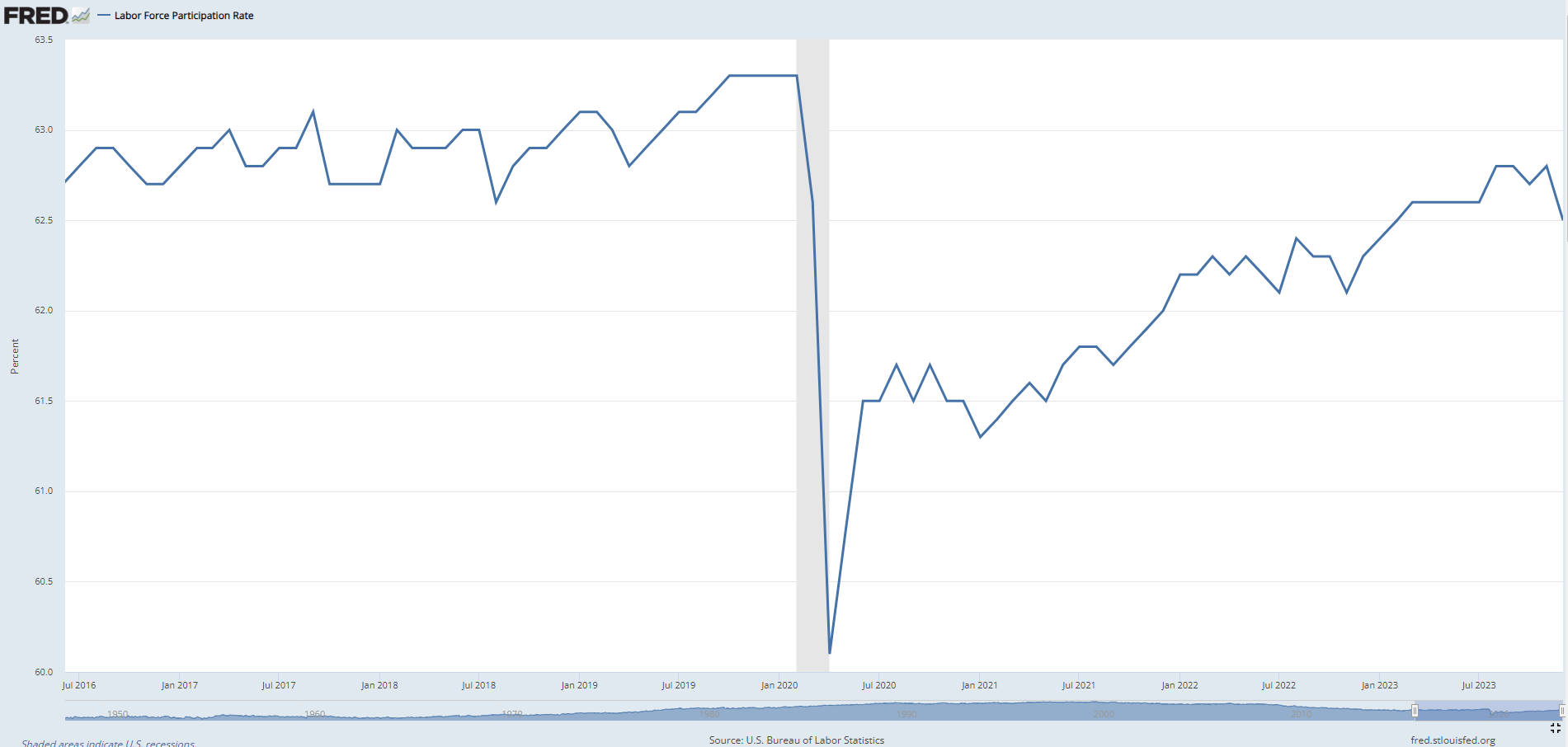

There has been much gnashing of teeth in recent weeks over how the unemployment rate would be exploding were it not for the recent decline in the labor participation rate (LPR) which fell -0.3% in December:

Source: St. Louis Fed (FRED)

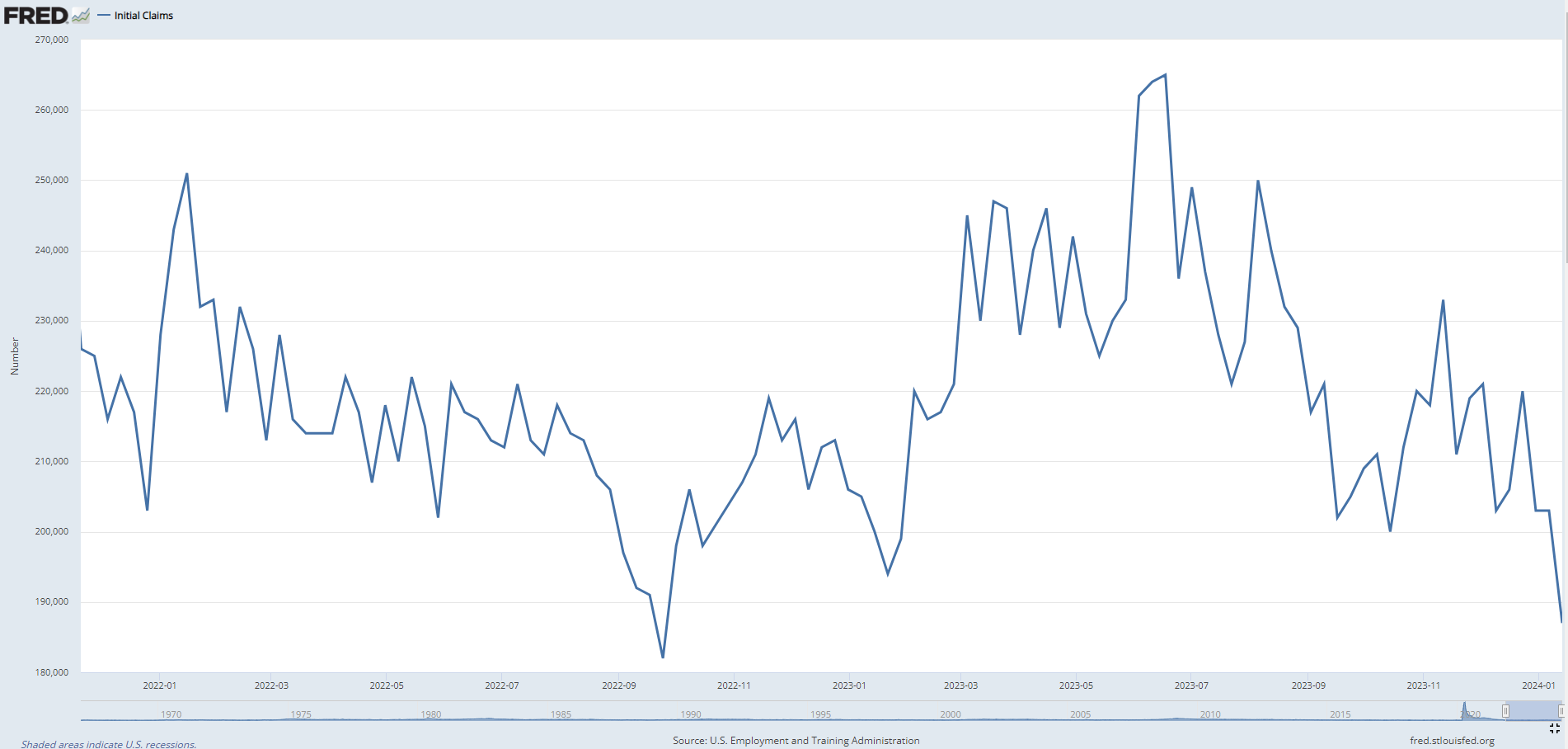

But I hear crickets on why initial jobless claims just…won’t…rip...

Source: St. Louis Fed (FRED)

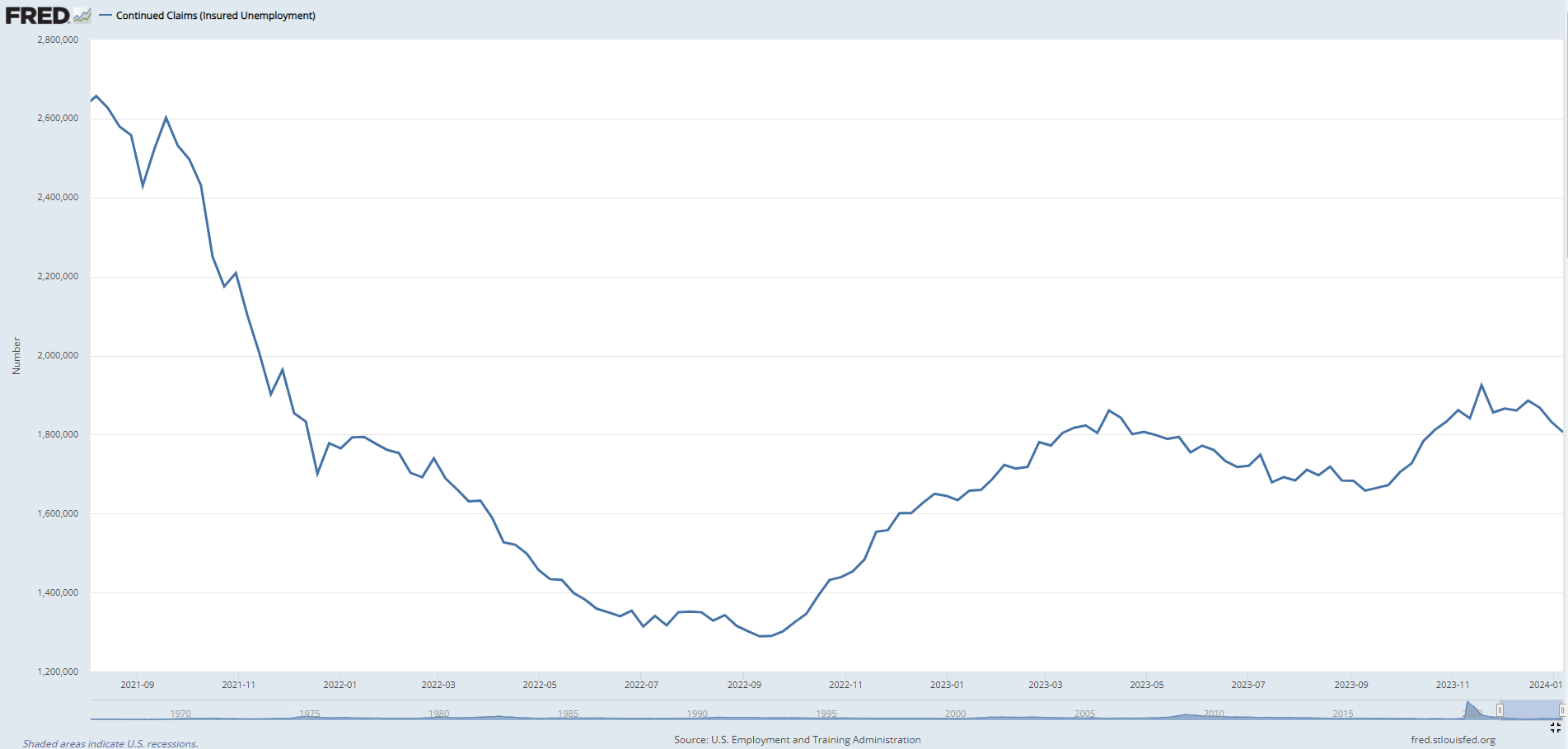

…and continuing claims ebb and flow but don’t spike:

Source: St. Louis Fed (FRED)

The popular explanation is that CEOs don’t want to relive the fire/rehire nightmare of the pandemic and will hold onto workers until they can’t preserve margins — and then the unemployment floodgates will open.

It makes me wonder if perhaps the potential workers everyone assumes are out there (“they’re unemployed but not accounted for — recession!!”) are actually gone because they can’t check the “willing and looking for work” box on their weekly unemployment filing?

Something else in the data caught my eye after scrolling farther down in the US Census data above — see the ages highlighted in blue?

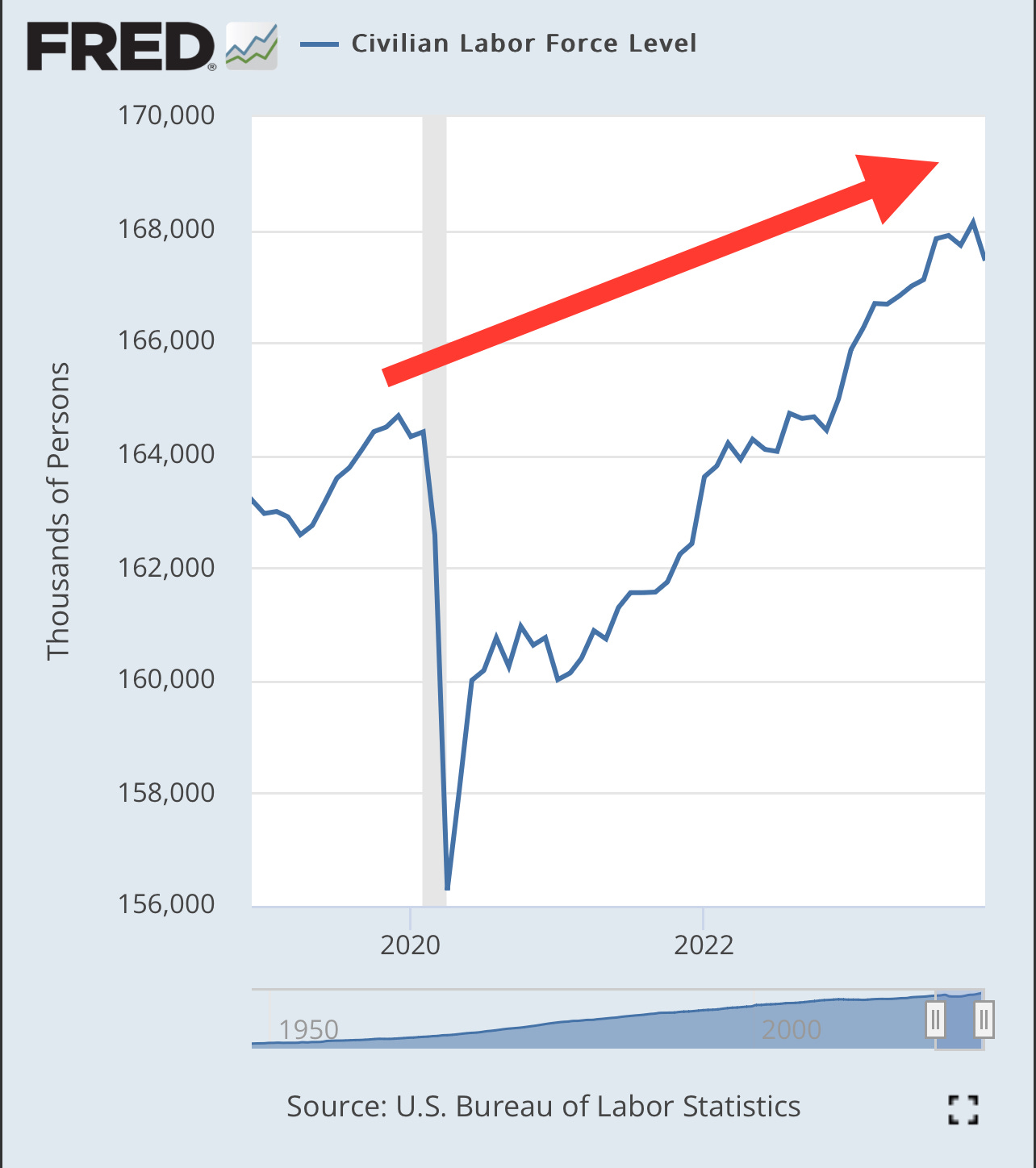

Perhaps a savvy reader can explain this to me, but it seems either Americans got frisky in the late 1990s, or otherwise embraced significant immigration in this particular cohort, because the 22-25 population notably bumped higher to 4.5-4.8mn per year after a 3-year intermission of ~4.4mn. Considering most American undergrads enter the workforce around 22, there was a good 300k/yr bump over trend in the supply of college-educated youths entering the labor force over the past three years. Looking at the total labor force, that’s nearly 1mn additions just on an entry bump. This does not explain the whole labor force change since the pandemic lows of course, but it does explain about a third of the ~3mn in labor gains from the ~165mn pre Covid peak… that’s not nothing:

Source: St. Louis Fed (FRED)

But look again at that table and you see the 22-year old entry cohort drops back to trend ~4.3mn/yr, just as the Boomer Plateau hits 67 and you get 4mn+ Boomers hitting 65 each year for the next 8 years. Absent aggressive immigration, labor force growth could slow to a crawl from here, and it’s not necessarily because labor demand is cooling dramatically on the precipice of a recession (although in past decades that has been a big recessionary tell — see late 2019). I am not going to argue with the army of economists and tweeters deep in the details about how “high quality jobs from Silicon Valley and Wall Street are vaporizing!” or “waves of immigrants will suppress wages but those are also low paying jobs!” My points above are extremely simplistic, and I am not a demographics expert.

Interestingly, this article in Sunday’s WSJ mentioned Boomers in passing (with an embedded link back to a September article about labor supply and demographics), but does not go far enough in painting a complete picture.

Over the next few years, you will see 4mn+ Boomers leave the workforce each year. It’s tempting to assume “well sure, but 4mn+ are coming in at age 22 and immigration will pick up the rest.”

The issue is that these people are retiring — they are not getting sick or dying. Not yet anyway. That will come later.

Some fun facts:

Baby Boomers make up 21% of the population.

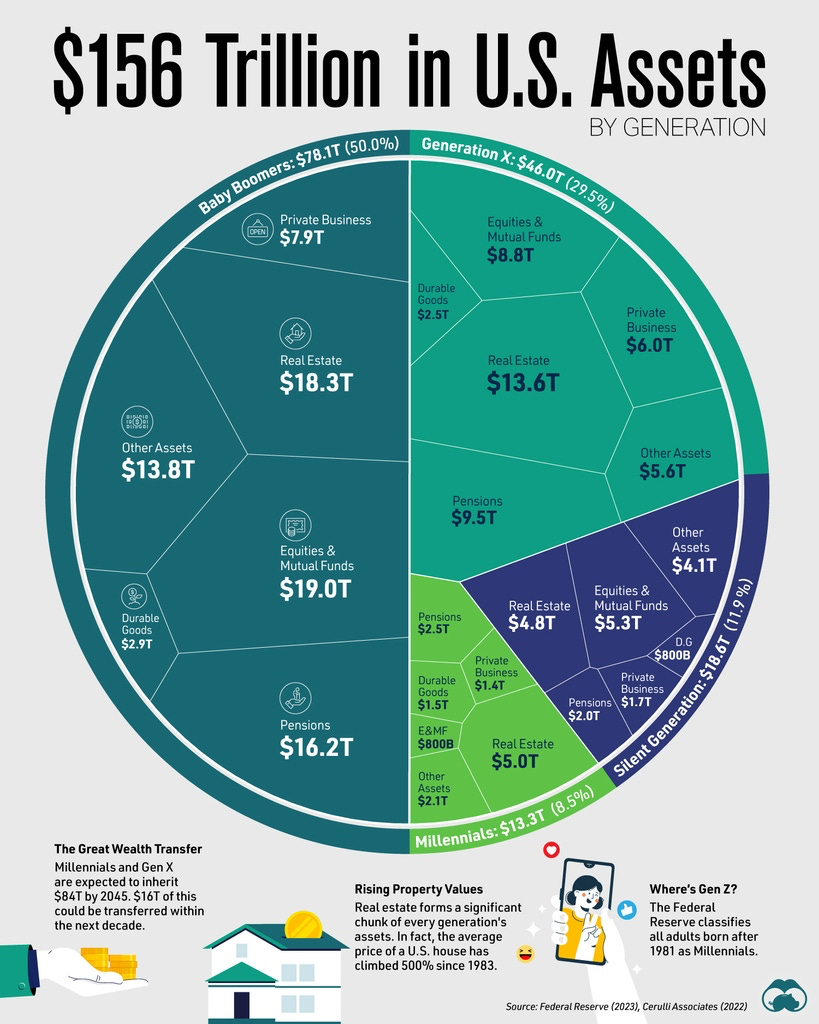

Baby Boomers control over 50% of US assets (link).

Baby Boomers are responsible for over half of US consumer spending (SeniorLiving.Org)

Source: VisualCapitalist.com

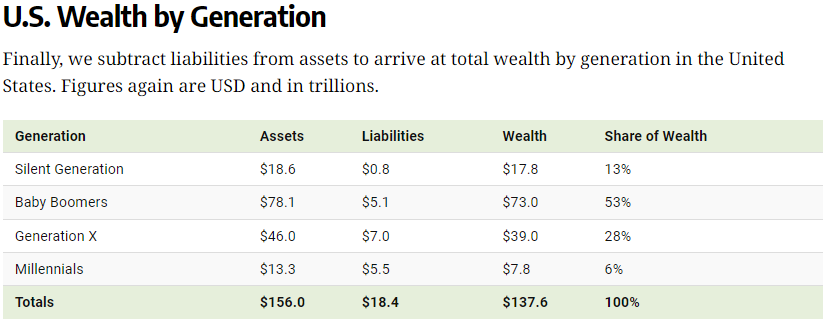

And when you factor in their net worth, the comparison vs Millennials (where liabilities exceed the Boomers) is truly stunning because Millennials are now the bigger cohort:

Source: VisualCapitalist.com

Stagnation in labor force growth while the consuming population presses onward is a gravitational pull higher on wages. Every Boomer retirement may be offset by an upcoming Gen Z’er, but they are both spending. And Boomers hold the savings while X/Millenials/Z holds the labor. One group pays, the other earns. And boy will they pay…I don’t care how tight you think financial conditions are or how lousy CEO sentiment is for hiring. If overall consumption is growing faster than labor supply, especially in a reshoring world, the prices of labor and therefore goods/services are going up.

This is your radio hiss in the economic universe, and this is happening now — not in five or ten years.

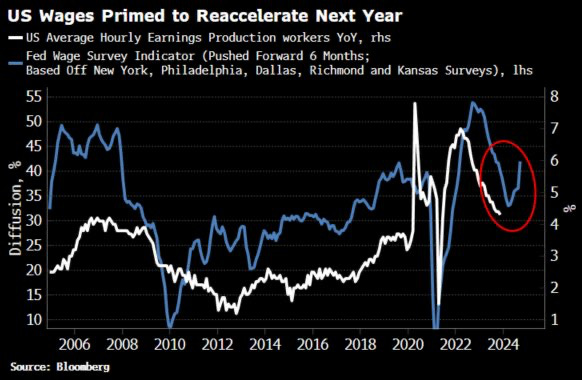

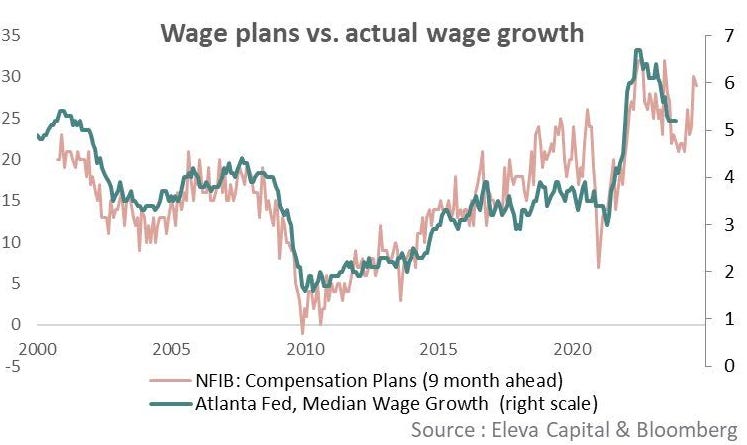

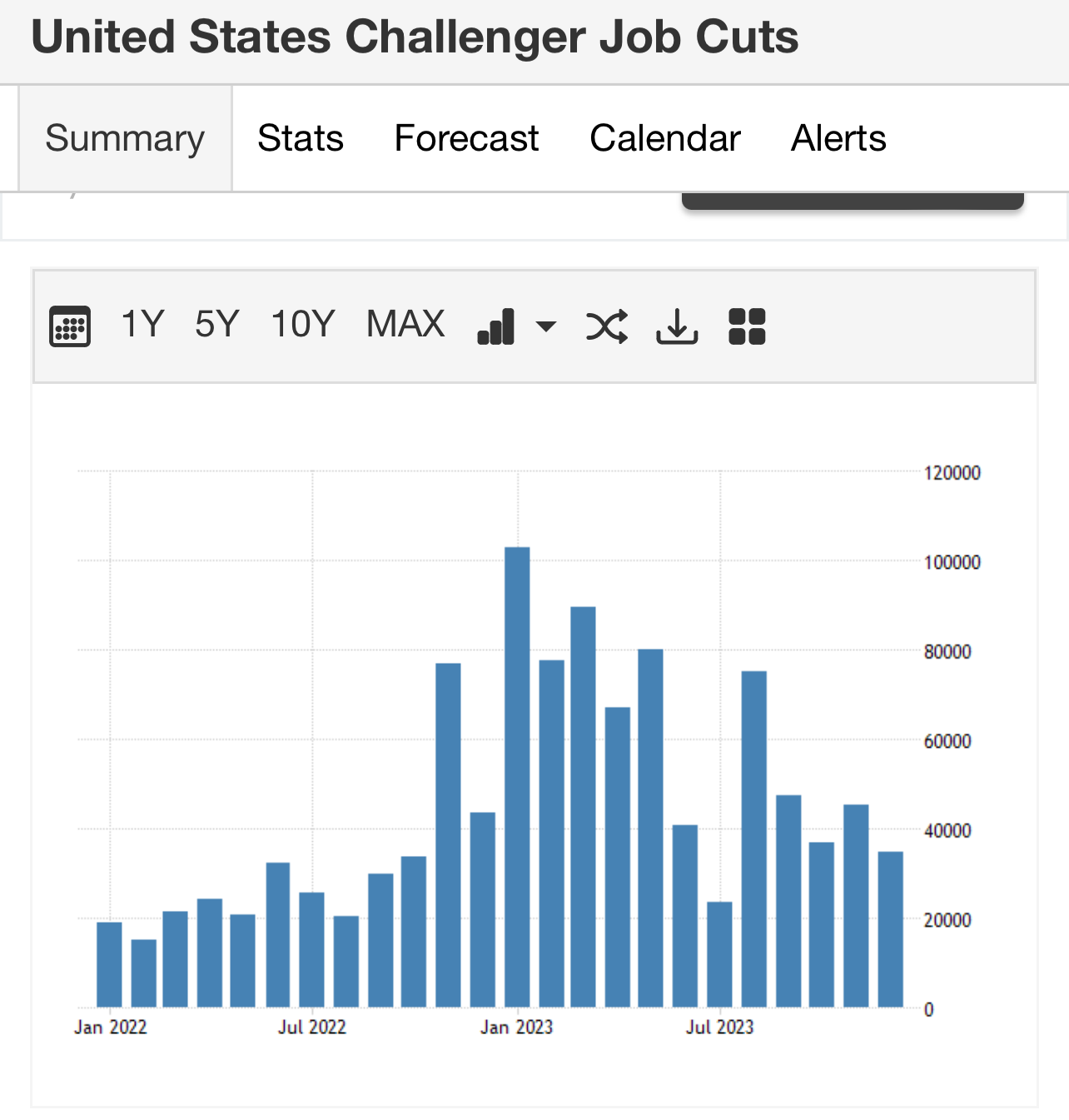

I know I harped on and on about sticky wages, inflections, and a Second Inflation Wave on Twitter in recent months despite tightened financial conditions and employment conditions loosening on the margin. But given the above, is it any surprise we see data like this?

Source: Federal Reserve of Atlanta

Source: Bloomberg

Source: Eleva Capital, Bloomberg

Source: TradingEconomics.com

Policymakers see this — “labor conditions are loosening but still pretty tight,” etc. But when you combine this backdrop with US Real Personal Income (+1.9% YoY) and Real Disposable Personal Income (+4.3% YoY) which flipped positive YoY a year ago and are inflecting higher as inflation slowed in 2023…

Source: St. Louis Fed (FRED)

… you realize just how risky the Fed’s talk of rate cuts and ending QT is. Policymakers seem hyper-focused on coincident/lagging indicators, rearview disinflation, and lower consumer inflation expectations from soft data surveys (UMich) that stem from the huge break consumers caught over the past 18 months with cheaper energy. Factor in 6%+ nominal GDP with enormous pro-cyclical fiscal deficits still working their way into the python from past earmarks, funded from previously sequestered reserves (RRP→Tbills discussed at length last summer on my TwitterX — remember my “no liquidity suck” months before bros became QRA experts?), and you have the prospect of an economy doing exactly what political incumbents would rejoice over: *running hot* by 3Q, just in time for elections.

None of this is necessarily new, but it means the Fed is possibly on the edge of yet another policy mistake — its third in 3 years (the first being Transitory in 2021, the second being the shallowed angle of attack in late 2022). Only this time the risk of overheating from loosened financial conditions hits late cycle. We can argue there is only so much they can do in the new normal of US fiscal dominance. But such a policy mistake could shake the tree hard for current trends in Large caps vs Small-midcap, Growth vs Value, Defensives (tech / healthcare) vs Cyclicals (commodities / consumer / industrials), Long vs Short Duration, and DM vs EM.

In my positioning discussion “Inflation Hedge Bros are Coming” a few weeks ago, I laid out why I think the market is nowhere near priced for such a prospect. Given the extended nature of current conditions, such a rotation could unfold in weeks or months rather than quarters or years (although both may ultimately prove true).

The risk I have been wrestling with is what if Passive, Mag7, & Nasdaq just continues to eat equity market flow as the US runs hot? Certainly possible. But if the oxygen for Passive is labor growth which begets 401k/Target Date/Passive inflows (note contribution limit increases are not keeping up with wage growth, creating greater disposable income post-401k contributions), and Gen Z labor force entry is largely offset by Boomer exits starting now (and considering Gen Z incomes are lower than Boomers, smaller 401k inflows are perhaps matched or exceeded by Boomer liquidations)…then perhaps it is possible the oxygen starts to come out of the room for Passive, benefiting Active strategies? Wishful thinking on my part maybe, and exceedingly hard to handicap. Generational transitions are hard. And I am not fully convinced demographics force an immediate flow reversal right here in front of us… but we shouldn’t rule out this shift as another hiss in the universe that could suddenly get very loud on the radio in the next 2-3 years.

As always kindly yours,

Paulo aka Cloudbear

this is great man ... very useful and enjoyable.

Comment on the youth population - late 90s is when the big immigration push began for Y2K and the Internet boom. Went full speed until it was slowed down a bit after 9/11. Bunch of those were from India and everybody knows our procreation abilities. All those kids will be in their 20s now.